International investment remains a critical, and often underappreciated, part of the global economy. Nearly two million jobs were created directly by foreign direct investment (FDI) in 2015, according to a Financial Timesanalysis. These employment gains in turn support many more jobs indirectly and, as a new paper from the Global Alliance for Trade Facilitation points out, can lead to productivity improvements throughout the wider economy.

International investment remains a critical, and often underappreciated, part of the global economy. Nearly two million jobs were created directly by foreign direct investment (FDI) in 2015, according to a Financial Timesanalysis. These employment gains in turn support many more jobs indirectly and, as a new paper from the Global Alliance for Trade Facilitation points out, can lead to productivity improvements throughout the wider economy.

The unbundling of modern production into regional and global value chains provides opportunities for economies to attract investments specialised in specific segments of the manufacturing chain. Morocco, for instance, has attracted over US$3bn in FDI into its

manufacturing sector since 2011, about two thirds of this into automotive components. Sri Lanka – another lower middle income country – attracted over $1bn in manufacturing FDI over the same period across a number of sectors focused on export markets. During this period, FDI into manufacturing accounted for less than one third of total investment in Sri Lanka, but more than two thirds of total jobs created by foreign investment.

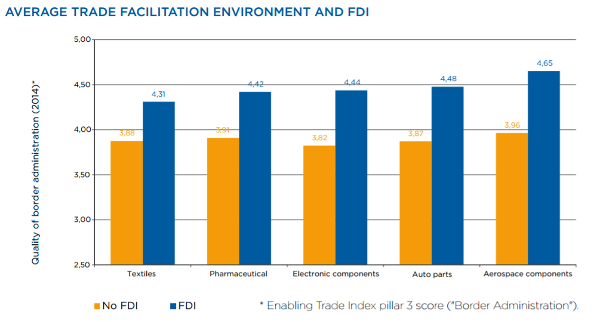

Only 5% of FDI into Africa goes into manufacturing, but even with the limited levels of FDI into this sector, it has been a major driver of formal employment in countries such as Ethiopia, Tanzania and Uganda. A number of factors drive the complex foreign investment decision-making process, but the ability of manufacturers to move goods quickly across borders is critical, especially for modern value chains.

A joined-up approach

Investment promotion agencies – key players in facilitating investment into priority sectors – must make the link between trade and investment. Similarly, customs and border agencies must understand the impact that improving service delivery has on productive sectors. Ambitious implementation of the WTO Trade Facilitation Agreement (TFA) – which came into force in February – sends a clear signal to both domestic and international investors that countries are committed to making trade easier and will prove influential in unlocking FDI opportunities, especially in the context of growing south-south trade and investment ties.

African countries are investing heavily in trade facilitation projects aimed at accelerating the movement of goods. This is a difficult task and a fine balancing act as they also have to preserve and secure government revenue. Yet, to maximise the yield of these investments, successfully achieve TFA objectives, and in the end increase FDI – it is essential that such projects are implemented in a coordinated, structured and sustainable way. It is for this reason that the Global Alliance for Trade Facilitation and other similar initiatives have been established. A lot of work still needs to be undertaken but Africa is moving in the right direction.

Philippe Isler is the executive director for the Global Alliance For Trade Facilitation and is based at the World Economic Forum in Geneva. This article was originally published by the World Economic Forum.

No comments:

Post a Comment